March was a difficult month for markets, as conflict with Iran cast a shadow over the first quarter. Following U.S. and Israeli strikes against Iran launched Feb 28, oil prices surged and bond yields moved higher, creating a challenging backdrop for both stocks and bonds. [1]

Only on the final trading day of March, when talk of an end to the war emerged (which ultimately did not last), did buyers return in force.[2] That helped markets finish off their worst levels for the month. The S&P 500 ended March down 5.1% and gave back nearly the last seven months of gains.[3],[4] Energy was the only one of the S&P 500’s eleven sectors to post a gain for the month.[5]

Source: https://www.wsj.com/finance/stocks/wall-street-is-finishing-the-worst-quarter-for-stocks-in-four-years-31ac41ea?mod=finance_lead_story

For the 1st quarter, the S&P 500 fell 4.6% — its weakest quarterly performance since 2022.[6] Technology stocks faced steeper declines, while small caps held up better, with the Russell 2000 still up for the quarter.[7]

Consumer discretionary and financial stocks were among the weaker performers in March, prompted by caution about the potential impact on spending and growth.[8] Investors who sought shelter in bonds and gold found that those traditional havens also pulled back alongside equities.[9]

Strait Jacket of Hormuz

Source: https://www.wsj.com/finance/commodities-futures/iran-war-stock-market-charts-cd95f497?mod=WTRN_pos1

The Strait of Hormuz is a narrow waterway that sits between Iran and Oman, connecting the Persian Gulf to the open ocean. Around 20% of global oil typically passes through it, but Iran effectively closed this passage following the outbreak of the war.[10] This standstill has become the largest oil supply disruption in recorded history, according to the International Energy Agency.[11]

Source: https://www.reuters.com/business/us-consumer-sentiment-slips-three-month-low-march-2026-03-27/

Since the conflict began, companies across industries, from airlines and trucking to agriculture, have begun planning for higher fuel costs, adding uncertainty to the economic outlook.[12] According to the American Automobile Association, the average price at the pump is almost $4 per gallon, up 35% in a month. In California, we can only dream of gas at $4 per gallon.[13] The U.S. energy department indicated that gas prices are likely to remain elevated through mid-2027.[14]

A Patient Federal Reserve

With rising oil prices and supply chain disruptions affecting key commodities like aluminum, the Federal Reserve (Fed) seems far less likely to cut interest rates.[15]

When the Fed held its scheduled policy meeting on March 17-18, it left the target interest rate unchanged at 3.50%–3.75%, as widely expected.[16] Faced with a combination of higher energy-driven inflation and slowing global growth, the Fed decided to wait for more clarity before acting.

Fed Chair Powell captured the uncertainty plainly: “We have an energy shock of some size and duration. We don’t know what that will be.”[17] Towards the end of the month, he offered a more reassuring tone, noting that long-term inflation expectations remain well-anchored and that the current rate level is “a good place” to sit while monitoring developments.[18] Markets interpreted this as a signal that rate hikes are not the base case.

Before the war began, interest rate markets had priced in an 80% probability of two cuts by year-end.[19] By the end of March, those odds plummeted to less than 5%.[20] On top of that, investors weighed the possibility that war-related spending could widen government deficits, pushing Treasury bond yields higher (prices lower).[21] The bond market often moves rapidly, reflecting the difficulty of pricing an evolving and uncertain situation.[22] For the month, Treasuries posted a loss of 1.8%.[23]

Context Matters

In March, the Fed also updated its economic projections, revising GDP growth modestly higher to 2.4% for 2026 while raising its inflation forecast to 2.7%.[24]

Despite all the turbulence in financial markets, consumers have shown resilience. While consumer sentiment softened in March, the underlying financial position of U.S. households remains solid.[25]

Although sticker shock is still likely, energy and gasoline costs actually account for a relatively small share of overall consumer spending. According to the Bureau of Economic Analysis, energy-related goods made up just 2% of consumer expenditures in the fourth quarter of 2025 — an 80-year low outside the pandemic period.[26] For context, energy spending approached 4% of total expenditure in 2008 when oil hit a then-record high just below $150.[27] American household net worth also remains at historically high levels, providing a meaningful financial cushion.[28]

Looking Ahead

Source: https://www.reuters.com/markets/us/war-oil-shock-uncertainty-time-raise-us-equity-outlook-2026-03-26

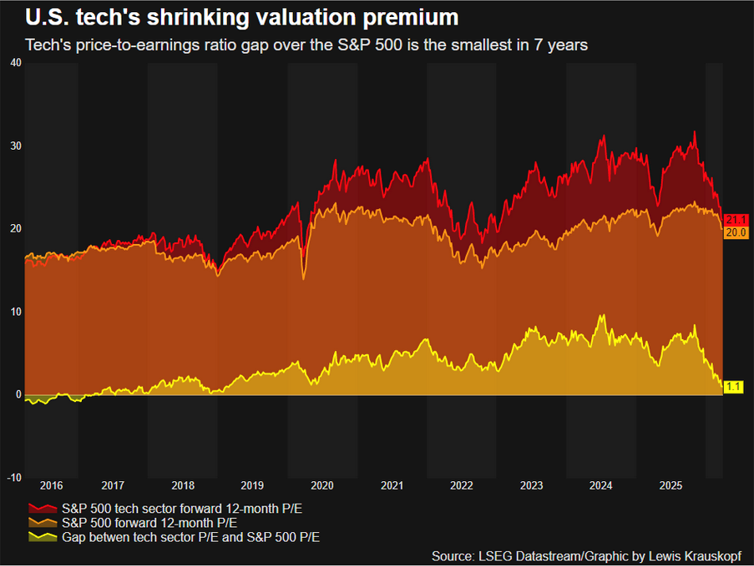

Earnings season kicks off again in April. Despite the pullback in the technology sector and lower valuations, its earnings are still expected to meaningfully outpace the broader market this year.[29] In fact, the valuation premium that technology has historically commanded over the rest of the market has narrowed to its smallest margin in roughly seven years.[30]

Although tech stock prices have come down, earnings growth estimates actually increased. LSEG consensus estimates place earnings growth at 42.5% for the technology sector in 2026, up from 30.8% at the start of the year and well above where those expectations stood six months ago.[31]

For the broader market, analysts also increased Q1 2026 earnings estimates during the first quarter — a reversal of the pattern over the last 20 years, in which estimates fell an average of 4.2%. If the current expected 13.2% year-over-year earnings growth rate holds, it would mark the sixth consecutive quarter of double-digit growth.[32] Corporate profitability remains a key engine for the market.

It’s worth pausing to appreciate how events on the other side of the world can impact our households, including through higher mortgage rates and gas prices. However, we have seen this pattern before: the disruption that feels unprecedented, knee-jerk reactions in markets, and the endurance of strategies that resist the urge to give in to the fear of the moment. Staying the course and rebalancing through a volatile market has historically served investors better.

We continue to use this period to review exposures, stress test allocations, and align your portfolio with your goals. Please be sure to keep us posted on any updates in circumstances and if you need any info or assistance in preparing your 2025 tax returns or payments. As usual, we’re happy to chat through any questions, the markets, or your plan. We look forward to more positive times, even if it becomes a longer road than expected.

From your friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, LLC. Neither JSF Financial LLC nor NewEdge Securities, LLC gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, LLC as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing. Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

TLT-iShares 20 Plus Year Treasury Bond ETF seeks to track the investment results of an index composed of US Treasury bonds with remaining maturities greater than twenty years.

The CBOE Volatility Index (VIX) is a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX). Because it is derived from the prices of SPX index options with near-term expiration dates, it generates a 30-day forward projection of volatility. Volatility, or how fast prices change, is often seen as a way to gauge market sentiment, and in particular the degree of fear among market participants.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] https://www.wsj.com/finance/stocks/wall-street-is-finishing-the-worst-quarter-for-stocks-in-four-ye…

[2] https://www.cnbc.com/2026/03/30/stock-market-today-live-updates.html

[3] https://www.cnbc.com/2026/03/30/stock-market-today-live-updates.html

[4] https://www.wsj.com/finance/stocks/wall-street-is-finishing-the-worst-quarter-for-stocks-in-four-ye…

[5] https://www.wsj.com/finance/stocks/wall-street-is-finishing-the-worst-quarter-for-stocks-in-four-ye…

[6] https://www.cnbc.com/2026/03/30/stock-market-today-live-updates.html

[7] https://www.cnbc.com/2026/03/30/stock-market-today-live-updates.html

[8] https://www.bloomberg.com/news/articles/2026-03-27/wall-street-reels-as-iran-war-shatters-its-portf…

[9] https://www.bloomberg.com/news/articles/2026-03-27/wall-street-reels-as-iran-war-shatters-its-portf…

[10] https://www.iea.org/news/new-iea-report-highlights-options-to-ease-oil-price-pressures-on-consumers…

[11] https://www.iea.org/reports/oil-market-report-march-2026

[12] https://www.ft.com/content/4b55d2eb-7231-4229-931f-0930d118f350

[13] https://www.reuters.com/markets/us/why-100-oil-wont-break-american-consumer-2026-03-23/

[14] https://www.ft.com/content/4b55d2eb-7231-4229-931f-0930d118f350

[15] https://www.wsj.com/finance/stocks/wall-street-is-finishing-the-worst-quarter-for-stocks-in-four-ye…

[16] https://www.federalreserve.gov/newsevents/pressreleases/monetary20260318a.htm

[17] https://www.usbank.com/investing/financial-perspectives/market-news/federal-reserve-interest-rate.h…

[18] https://www.cnbc.com/2026/03/30/powell-sees-inflation-outlook-in-check-no-wider-crisis-yet-in-priva…

[19] https://www.wsj.com/finance/stocks/wall-street-is-finishing-the-worst-quarter-for-stocks-in-four-ye…

[20] https://www.wsj.com/finance/stocks/wall-street-is-finishing-the-worst-quarter-for-stocks-in-four-ye…

[21] https://finance.yahoo.com/news/war-spending-sinks-long-term-094500001.html

[22] https://finance.yahoo.com/economy/policy/articles/global-bond-yields-climbing-iran-020505989.html

[23] https://www.bloomberg.com/news/articles/2026-03-31/muni-buyers-start-to-nibble-as-market-has-worst-…

[24] https://www.cnbc.com/2026/03/18/fed-interest-rate-decision-march-2026.html

[25] https://www.reuters.com/business/us-consumer-sentiment-slips-three-month-low-march-2026-03-27/

[26] https://www.reuters.com/markets/us/why-100-oil-wont-break-american-consumer-2026-03-23/

[27] https://www.reuters.com/markets/us/why-100-oil-wont-break-american-consumer-2026-03-23/

[28] https://www.reuters.com/markets/us/why-100-oil-wont-break-american-consumer-2026-03-23/

[29] https://finance.yahoo.com/markets/stocks/articles/nasdaq-100-enters-correction-falls-195640896.html

[30] https://www.reuters.com/markets/us/war-oil-shock-uncertainty-time-raise-us-equity-outlook-2026-03-2…

[31] https://www.reuters.com/markets/us/war-oil-shock-uncertainty-time-raise-us-equity-outlook-2026-03-2…

[32] https://insight.factset.com/sp-500-earnings-season-preview-q1-2026